The AAII weekly sentiment survey shows the promise of a market rally with caveats

I am using the American Association of Individual Investors weekly survey (bulls/bears/neutrals) as a contrarian indicator for market direction.

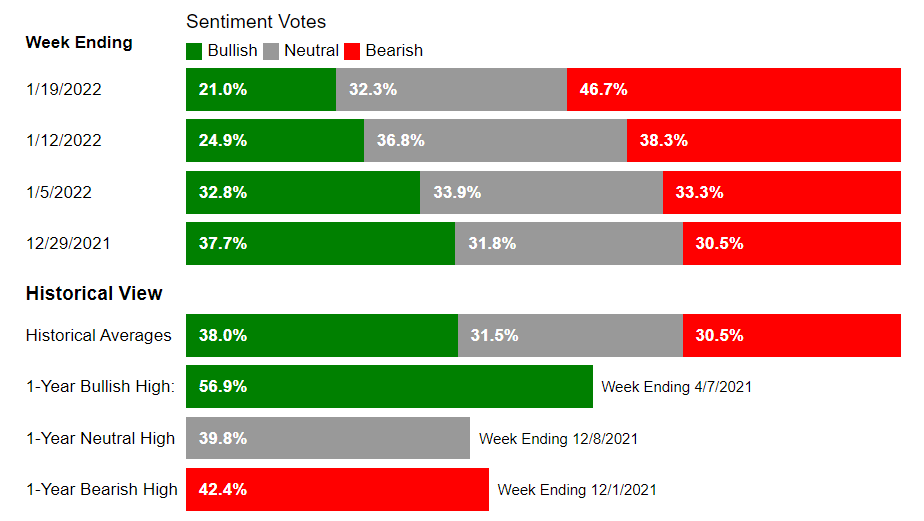

The AAII sentiment survey for the week ending January 19 is out:

Bullish sentiment fell 3.9 percentage points to 21%. Third week down. Lowest level since week ending July 30, 2020. 45% below the historical average. This is the biggest differential below the historical average since July 2020.

Neutral sentiment fell 4.5 percentage points to 32.3%. First decline in 3 weeks. Lowest level in 3 weeks. 4% above the historical average.

Bearish sentiment increased 8.4 percentage points to 46.7%. Third week up. Biggest increase in 5 weeks. highest levels since the week ending September 10, 2020. 53% above the historical average. This is the most above the historical average since September 2020.

Bullish sentiment at extreme low and bearish sentiment at extreme high. These are conditions for a rally, but momentum to the downside cannot be ignored. These sentiment readings may stay negative for a short while longer, but at some point a rally is likely.

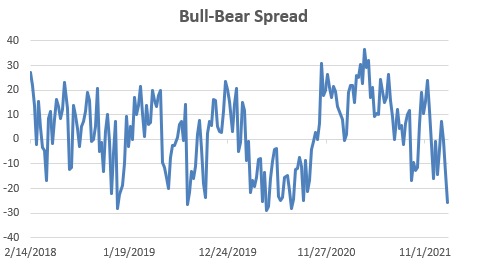

The Bull-Bear spread is -25.7. Third week negative and most negative since July 2020.

The massive OPEX this week adds an extra layer of complexity to any short term trend analysis as deep in-the-money options in single stocks are closed or rolled with different impact on the options market makers book composition.

The caveats mentioned in the title refer to the fragility of the bear consensus - any accommodating policy adjustment from the Fed, even some reassuring words from Powell during the press conference after the FOMC meeting next week could unleash the bulls back into the market. While the mainstream media chases headlines, the most important observation on the markets is the lack of breadth/weak liquidity. Coupled with the negative gamma dealers are carrying into Friday this produces conditions for unusually high volatility, more likely than not leveraged by institutional investors and large trading desks.

On a side note, Covid-19 cases are declining fast in countries such as UK, Ireland and the United States - a policy shift there in regards to social distancing, vaccines or travel restrictions will force the Fed to remain very flexible with the upcoming rate hikes and quantitative tightening. After all chair Powell retired the “transitory” phrase and signaled a hawkish Fed stance but nothing actually happened yet, so to keep in the contrarian style I expect the inflation to stabilize and supply to catch up with demand by June.